13 min read

'%3e%3cg%20clip-path='url(%23b6dc094121)'%3e%3cpath%20fill='%230066cc'%20d='M%2012.707031%205.710938%20L%2012.707031%2035.761719%20L%2037.007812%2035.761719%20L%2037.007812%205.710938%20Z%20M%2012.707031%205.710938%20'%20fill-opacity='1'%20fill-rule='nonzero'/%3e%3c/g%3e%3c/g%3e%3cg%20clip-path='url(%23cd2e57bbdf)'%3e%3cg%20clip-path='url(%23cc31bb2a50)'%3e%3cpath%20fill='%230066cc'%20d='M%2026.734375%201.035156%20L%2026.734375%2035.761719%20L%2036.882812%2035.761719%20L%2036.882812%201.035156%20Z%20M%2026.734375%201.035156%20'%20fill-opacity='1'%20fill-rule='nonzero'/%3e%3c/g%3e%3c/g%3e%3cg%20clip-path='url(%23ab469c456a)'%3e%3cg%20clip-path='url(%23fb318aa8dc)'%3e%3cpath%20fill='%230066cc'%20d='M%200.0546875%201.035156%20L%200.0546875%2035.761719%20L%2010.203125%2035.761719%20L%2010.203125%201.035156%20Z%20M%200.0546875%201.035156%20'%20fill-opacity='1'%20fill-rule='nonzero'/%3e%3c/g%3e%3c/g%3e%3cg%20clip-path='url(%238fe1ac7b9f)'%3e%3cg%20clip-path='url(%23f68e7172d0)'%3e%3cpath%20fill='%230066cc'%20d='M%200%205.710938%20L%200%2035.761719%20L%2024.269531%2035.761719%20L%2024.269531%205.710938%20Z%20M%200%205.710938%20'%20fill-opacity='1'%20fill-rule='nonzero'/%3e%3c/g%3e%3c/g%3e%3c/svg%3e)

At first glance, personal finance seems straightforward: earn more than you spend, save the rest. Yet, for countless individuals, truly knowing their numbers – understanding where every dollar goes and why – proves to be a surprisingly arduous task. This article delves into the complex layers that m

Yağız Gürbüz

Founder & CEO

🎧 En iyi deneyim için kulaklık kullanmanızı öneririz

At first glance, personal finance seems straightforward: earn more than you spend, save the rest. Yet, for countless individuals, truly knowing their numbers – understanding where every dollar goes and why – proves to be a surprisingly arduous task. This article delves into the complex layers that make mastering your money far harder than it initially appears, offering insights and actionable solutions.

The fundamental equation of personal finance – income minus expenses equals savings – presents itself with disarming simplicity. However, beneath this veneer lies a sprawling, intricate reality. What appears to be a basic math problem quickly spirals into a labyrinth of data points, making true mastery of one's financial situation a formidable challenge. The sheer volume and variety of transactions alone can overwhelm even the most diligent individual, transforming a simple budget into a complex data analysis project.

Consider the average person's financial life today. Between daily coffee runs, online subscriptions, grocery bills, utilities, loan repayments, and occasional discretionary spending, the number of individual transactions in a single month can easily run into the hundreds. Each of these micro-decisions contributes to the overall financial picture, yet tracking every single one manually becomes a monumental, often unsustainable, effort. Furthermore, these transactions often occur across multiple platforms: credit cards, debit cards, bank transfers, digital wallets, and even dwindling cash payments. Consolidating and categorizing this disparate data requires significant time and attention, often leading to a sense of being perpetually behind or simply guessing at the true figures.

The challenge intensifies for those with irregular income streams, such as freelancers, gig workers, or commission-based employees. Without a fixed monthly salary, budgeting becomes a dynamic, constantly shifting target. One month might bring a windfall, while the next could see a significant dip, making consistent saving and spending plans incredibly difficult to maintain. Similarly, variable expenses pose a significant hurdle. While rent or mortgage payments are typically fixed, costs like utilities (especially with seasonal changes), groceries (affected by prices and dietary needs), car maintenance, healthcare, and entertainment fluctuate wildly. These unpredictable elements make it nearly impossible to create a static budget that accurately reflects reality month after month, leading to frequent budget overruns or underspending that throws off long-term financial planning.

In an attempt to simplify, many individuals fall into the trap of relying on averages and estimates rather than precise data. "I spend about $500 on groceries" or "My utilities are usually around $150" are common approximations. While these rough figures might seem sufficient for a general overview, they often mask significant discrepancies and prevent a true understanding of where money is actually going. Averages can hide spending spikes in certain categories, or fail to account for infrequent but substantial expenses like annual insurance premiums or car repairs. Without precise tracking and categorization, individuals operate under an illusion of control, believing they know their numbers when, in reality, they are navigating their finances with a blurry, inaccurate map. This lack of detailed knowledge means opportunities for optimization and savings are frequently missed, as the specific areas for improvement remain hidden beneath generalized figures.

Beyond the practical complexities, human psychology plays a profoundly powerful role in making personal finance mastery elusive. Our brains, wired for immediate gratification and often susceptible to various cognitive biases, frequently sabotage our best intentions for rational and consistent money management. Understanding these psychological hurdles is crucial for developing strategies to overcome them.

One of the most potent psychological barriers is emotional spending. Whether it's retail therapy to alleviate stress, celebratory splurges after a success, or impulse buys driven by boredom or social media influence, emotions often dictate purchasing decisions more than logical financial planning. The desire for instant gratification, a deeply ingrained human tendency, further complicates matters. Saving for a distant goal like retirement or a down payment requires delaying pleasure, a concept that often clashes with our innate drive for immediate rewards. The dopamine hit from a new purchase can feel more tangible and satisfying in the moment than the abstract concept of future financial security, leading to spending habits that undermine long-term financial health.

Our financial decisions are heavily influenced by a range of cognitive biases. Present bias, for instance, leads us to overvalue immediate rewards and undervalue future ones. This explains why people struggle to save for retirement, preferring to spend now rather than invest for decades down the line. Another common bias is mental accounting, where we treat different pots of money differently, even though money is fungible. For example, people might be extremely frugal with their salary but readily splurge on "found money" like a tax refund or a bonus, failing to integrate it into their overall financial strategy. Similarly, the sunk cost fallacy can lead individuals to continue investing in a failing venture (be it a stock or a hobby) simply because they've already put so much into it, rather than cutting their losses. These biases distort our perception of value and risk, making purely rational financial decision-making incredibly challenging.

The act of tracking one's finances can itself be emotionally and mentally taxing. For many, confronting bank statements and expense logs means facing uncomfortable truths about spending habits, past mistakes, or current financial limitations. This 'pain of tracking' can lead to avoidance. Furthermore, the sheer mental effort required to consistently categorize transactions, balance budgets, and review statements can lead to what's known as financial fatigue. After a long day, the last thing many people want to do is sit down and meticulously review their spending. This fatigue can result in procrastination, skipped tracking sessions, and ultimately, a loss of control over one's financial narrative. The perceived drudgery outweighs the perceived benefit, especially when the benefits of good financial habits are often long-term and not immediately apparent.

Perhaps the most insidious psychological barrier is the tendency towards procrastination and outright avoidance, often termed the 'head in the sand' approach. When faced with financial stress, debt, or simply the overwhelming task of getting organized, it's easier to simply ignore the problem. This avoidance manifest in delaying bill payments, not opening bank statements, or refusing to look at credit card balances. While providing temporary relief from anxiety, this strategy invariably exacerbates the underlying issues, leading to late fees, increasing debt, and a growing sense of helplessness. The fear of what one might find often prevents people from looking at all, creating a vicious cycle where ignorance fosters greater financial instability.

While personal finance challenges often feel intensely individual, many external and systemic factors significantly complicate the journey to financial mastery. These societal and economic forces create an environment where even with the best intentions, individuals face an uphill battle in managing their money effectively.

One of the most significant systemic issues is the widespread lack of formal financial education. Most educational systems historically have not prioritized teaching practical money management skills, leaving individuals to learn about budgeting, saving, investing, debt management, and financial planning through trial and error, often after making costly mistakes. Many adults enter the workforce with little to no understanding of how to read a pay stub, manage credit, or plan for retirement. This knowledge gap means that financial decisions are often made from a position of ignorance, rather than informed choice. Parents, who may themselves lack comprehensive financial literacy, often struggle to impart these crucial skills to their children, perpetuating a cycle of financial vulnerability across generations. Without a foundational understanding, even basic financial concepts can seem daunting and inaccessible.

The financial landscape has grown exponentially more complex in recent decades. Gone are the days of simple savings accounts and basic mortgages. Today, consumers are bombarded with an bewildering array of financial products and services: high-yield savings accounts with tiered interest rates, complex investment vehicles like ETFs, cryptocurrencies, and fractional shares, variable-rate mortgages, student loans with intricate repayment plans, credit cards with nuanced reward structures and hidden fees, and an explosion of fintech apps. Understanding the terms, conditions, risks, and benefits of each product requires significant research and a degree of financial sophistication that many simply do not possess. This complexity can lead to poor choices, falling prey to predatory lending, or simply being too intimidated to engage with essential financial tools like investing, thereby missing out on significant wealth-building opportunities.

Societal pressures and the pervasive influence of social media exacerbate the challenge of mastering personal finance. The phenomenon of "keeping up with the Joneses" has evolved from comparing oneself to neighbors to comparing oneself to a curated, often unrealistic, highlight reel of others' lives online. Constant exposure to aspirational lifestyles, expensive purchases, and luxurious experiences can foster a sense of inadequacy and a powerful urge to spend beyond one's means. This pressure can manifest in impulse purchases, taking on unnecessary debt for status symbols, or prioritizing consumption over saving. The desire for social acceptance and the fear of missing out (FOMO) can override rational financial planning, making it incredibly difficult to stick to a budget when perceived societal norms dictate otherwise.

Another profound systemic challenge is inflation, which constantly erodes the purchasing power of money. While often discussed in abstract economic terms, inflation has a very real, tangible impact on personal finances. What $100 could buy last year might only buy $95 worth of goods and services this year. This means that merely saving money isn't enough; one must invest it wisely to ensure its growth outpaces inflation. For those who don't understand or actively manage their investments, inflation acts as a hidden tax, silently diminishing their wealth over time. Moreover, the unpredictable nature of inflation, often driven by global economic forces, turns financial planning into a moving target. Long-term goals like retirement savings or buying a home require constant adjustment to account for the increasing cost of living, adding another layer of complexity to financial mastery.

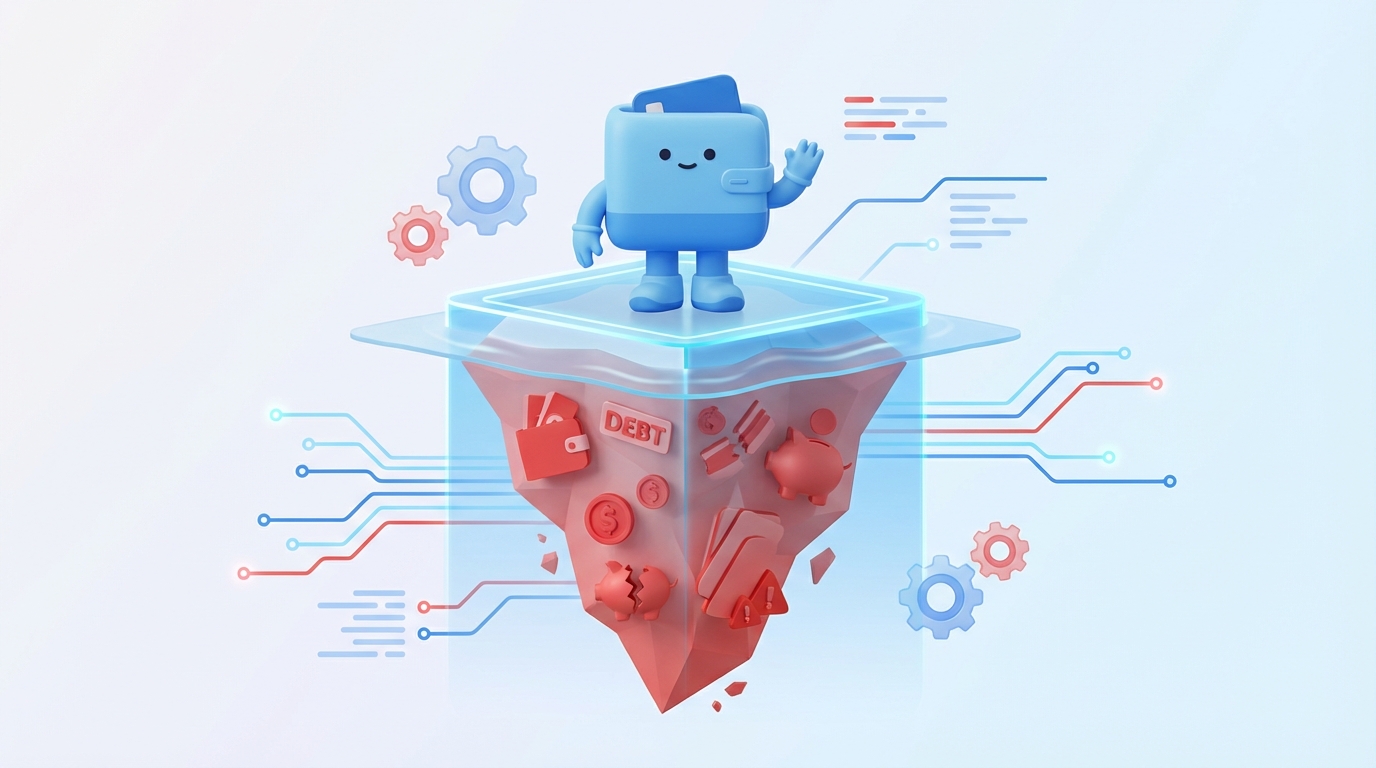

The failure to truly master one's personal finance numbers carries significant, often hidden, costs that extend far beyond mere inconvenience. These consequences can profoundly impact an individual's financial stability, emotional well-being, and ability to achieve life goals, creating a ripple effect that touches nearly every aspect of their existence.

Perhaps the most direct financial cost of not knowing your numbers is the myriad of missed opportunities for growth and savings. Without a clear understanding of cash flow, spending patterns, and available funds, individuals often fail to identify areas where they could cut unnecessary expenses, optimize recurring bills, or negotiate better deals. More significantly, a lack of financial insight means missing out on the power of compounding interest. If you don't know how much you can realistically save each month, or where to invest those savings, you forgo years of potential growth. This could mean missing out on maximizing employer matching contributions in retirement accounts, failing to take advantage of high-yield savings accounts, or simply leaving money dormant in low-interest checking accounts when it could be actively working for you. These missed opportunities compound over time, leading to substantially less wealth accumulation in the long run.

A murky financial picture is a breeding ground for unnecessary debt. When individuals don't accurately track their spending, it's easy to gradually spend more than they earn, leading to reliance on credit cards or loans to bridge the gap. This often happens subtly, with small overspends accumulating into significant balances. The true cost of this debt is not just the principal amount, but the exorbitant interest payments that accrue over time. Credit card interest rates, often in the double digits, can turn a seemingly small purchase into a much larger expense over months or years. Not knowing your numbers means you might not realize the true cost of your debt, or how quickly it's growing, until it becomes an overwhelming burden. This cycle of debt can make it incredibly difficult to save, invest, or achieve any other financial goal, essentially paying for past consumption at the expense of future prosperity.

The emotional and psychological toll of financial uncertainty is immense. Not knowing where you stand financially – living paycheck to paycheck, worrying about unexpected expenses, or facing mounting debt – is a leading cause of stress and anxiety. This constant worry can impact mental health, sleep quality, and overall well-being. Furthermore, financial issues are a primary source of conflict in relationships. When one or both partners lack a clear understanding of their shared finances, it can lead to arguments, distrust, and resentment. Disagreements over spending habits, saving priorities, or hidden debt can erode the foundation of a relationship, highlighting how deeply personal finance intertwines with emotional and relational health. The stress of financial instability can permeate every aspect of life, making it difficult to focus on work, enjoy leisure time, or maintain healthy personal connections.

Ultimately, the most significant long-term cost of not mastering your personal finance numbers is the delay or outright failure to achieve crucial life goals. Whether it's saving for a comfortable retirement, buying a first home, funding a child's education, starting a business, or taking a dream vacation, all these aspirations require meticulous financial planning and consistent execution. Without a clear financial roadmap, accurate budgeting, and disciplined saving, these goals remain distant dreams rather than achievable milestones. A lack of understanding about how much needs to be saved, by when, and how to invest it effectively means that individuals often find themselves perpetually behind schedule, or realizing too late that their goals have become financially out of reach. This can lead to profound disappointment and a diminished quality of life in later years, underscoring the critical importance of financial literacy and control.

Overcoming the inherent challenges of personal finance mastery requires a proactive and strategic approach. Fortunately, there are many practical strategies and tools available to help individuals demystify their finances and gain real control over their money.

One of the most powerful strategies is to automate as much of your financial life as possible. This removes the need for constant manual intervention and leverages consistency. Set up automatic transfers from your checking account to your savings and investment accounts immediately after your paycheck hits. Even small, consistent contributions add up significantly over time thanks to the power of compounding. Similarly, automate bill payments for recurring expenses like rent, utilities, loan repayments, and subscriptions. This ensures bills are paid on time, avoiding late fees and credit score damage. Automation turns good financial habits into default actions, reducing the mental effort and willpower required, and protecting you from your own psychological biases.

There is no one-size-fits-all solution for tracking finances; the best tool is the one you will actually use consistently. Explore various options to find what fits your personality and lifestyle.

Once you have a tracking tool, the crucial next step is to consistently categorize your spending and regularly review your financial data. This transforms raw numbers into actionable insights. Instead of just seeing "shopping," categorize it as "groceries," "clothing," or "entertainment." This level of detail allows you to identify exactly where your money is going and pinpoint areas for adjustment. Schedule dedicated time each week or month to review your budget, compare actual spending to planned spending, and adjust as needed. Make this a non-negotiable habit, like brushing your teeth. Frame it as an empowering act of control rather than a tedious chore. Regular reviews help catch issues early, celebrate progress, and keep your financial goals top-of-mind.

While detailed tracking is important, it's also crucial not to get bogged down in every single penny, which can lead to financial fatigue. Instead, focus on a few key metrics that provide a high-level overview of your financial health.

You don't have to navigate the complexities of personal finance alone. For significant financial decisions, complex investment strategies, or when feeling overwhelmed, seeking professional guidance can be invaluable.

Achieving true mastery over your personal finance numbers is not a one-time event but an ongoing journey. It requires developing sustainable habits, continuous learning, and a resilient mindset to navigate the inevitable ups and downs of financial life. Building a lasting financial understanding means integrating these practices into your daily life.

Consistency is the bedrock of long-term financial success. Just as you have routines for work, exercise, or self-care, establish a regular financial routine. This might involve:

The financial world is constantly evolving, with new products, regulations, and economic trends emerging regularly. Therefore, continuous financial education is paramount.

The path to financial mastery is rarely linear. There will be setbacks, unexpected expenses, moments of emotional spending, and perhaps even some poor investment decisions. It's crucial to approach these moments with patience and self-compassion. Instead of dwelling on mistakes or becoming discouraged, view them as learning opportunities. Understand that financial behavior change takes time, and perfection is an unrealistic expectation. Forgive yourself for past missteps, learn from them, and recommit to your goals. A resilient mindset, one that acknowledges challenges without letting them derail progress, is essential for sustainable financial health.

To maintain motivation and reinforce positive financial behaviors, make sure to celebrate your progress, no matter how small. Did you stick to your budget for a month? Did you pay off a small debt? Did your net worth increase by a modest amount? Acknowledge these achievements. Celebrating doesn't mean splurging and undoing your hard work; it can be as simple as treating yourself to a small, planned reward, sharing your success with a supportive friend, or simply taking a moment to appreciate how far you've come. These positive reinforcements help to associate good financial habits with positive feelings, making the journey more enjoyable and sustainable in the long run.

Mastering your personal finance numbers is undeniably a complex undertaking, extending far beyond simple arithmetic. It involves navigating the illusion of simplicity created by countless transactions and fluctuating incomes, overcoming deep-seated psychological barriers that push us towards instant gratification and avoidance, and contending with systemic challenges like inadequate financial education and an increasingly complex economic landscape. The hidden costs of ignoring these complexities are substantial, leading to missed opportunities, accumulating debt, increased stress, and ultimately, unachieved life goals. However, by embracing practical strategies such as automation, utilizing the right tools, establishing consistent routines, continuously educating oneself, and practicing self-compassion, anyone can demystify their finances. Building a sustainable financial understanding is a journey of continuous learning and adaptation, empowering individuals to take control of their money, reduce stress, and confidently work towards a secure and fulfilling financial future.

Written by

Founder & CEO

Sharing knowledge on personal finance, budget management, and investment strategies to help you achieve financial freedom.